A Simple Way to Manage Your Money

If you’ve ever searched for a straightforward way to organise your finances, you’ve probably come across the 50/30/20 budgeting rule. It’s often described as one of the simplest budgeting frameworks available — and for good reason.

At the core, the 50/30/20 budgeting rule is a simple way to manage your money. It helps you better understand your spending. It gives structure to your income without requiring complicated spreadsheets or daily expense tracking. In this guide, we’ll break down exactly how it works, where it can be helpful, where it may fall short, and how to use it responsibly.

This is general financial education designed to help you understand the framework — not a personal recommendation. Every household’s circumstances differ, and the percentages are best viewed as guidelines rather than rigid rules.

What Is the 50/30/20 Budget Rule?

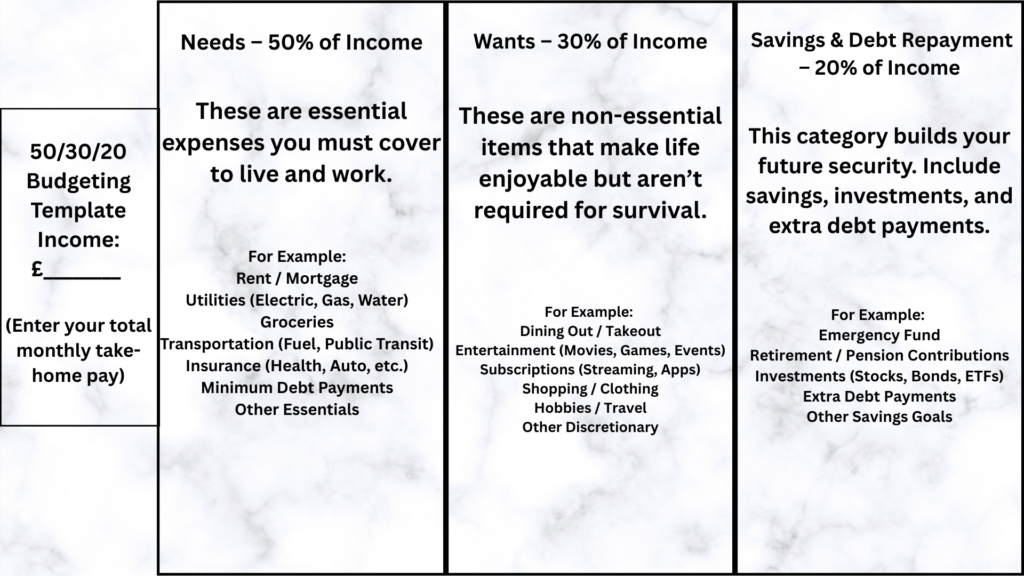

The 50/30/20 budgeting rule is a method that divides your after-tax (take-home) income into three broad categories:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Debt Repayment

It was popularised in the United States by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, in their book called *All Your Worth: The Ultimate Lifetime Money Plan*. This rule helps people manage their money. It suggests splitting your after-tax money into three parts: 50% for needs (like food and a place to live), 30% for wants (like fun activities and hobbies), and 20% for saving or paying off debts.

It is easy to understand because instead of watching many different categories, you only focus on these three parts. The 50/30/20 budgeting rule is fundamentally a simple method to manage money. By using this strategy, people can budget their money better and work towards a stable financial future.

Let’s break them down.

1. The 50% – Needs

These are essential expenses required to maintain your basic standard of living. Typically, this includes:

- Housing costs (rent or mortgage payments)

- Utilities

- Council tax

- Basic groceries

- Insurance

- Transport necessary for work

- Minimum debt repayments

If you lost your income tomorrow, these are the expenses you’d struggle to avoid.

2. The 30% – Wants

Wants are discretionary. They enhance your lifestyle but aren’t strictly essential. For example:

- Eating out

- Holidays

- Streaming subscriptions

- Gym memberships

- Upgraded phone plans

- Hobbies and leisure spending

The purpose of including “wants” in a budget is not to eliminate enjoyment, but to ensure lifestyle spending remains intentional rather than automatic.

3. The 20% – Savings and Debt Reduction

This 20% portion is directed toward improving your financial position over time. It may include:

- Building an emergency fund

- Long-term investing

- Pension contributions

- Overpaying high-interest debt

- Other long-term financial goals

The emphasis here is future stability and growth.

How the 50/30/20 Rule Works in Practice

The concept is simple. Applying it in real life requires more nuance.

Step 1: Calculate Your Net Income

The key point to understand here is that the focus should be on the net income you receive once you’ve accounted for all necessary deductions. It’s important to think about not just the money you take home after taxes, but also other regular costs. These costs include National Insurance, pension savings, and any extra payments you may have. To really understand your finances, you should look at how much money you have left after all these expenses are deducted.

If your income varies from month to month—like if you’re self-employed or earn commissions—it might be better to look at an average over a few months to get a clearer idea of your usual earnings.

Step 2: Categorise Your Spending Honestly

This is often where the learning happens. Many people underestimate how much falls into “wants” rather than “needs.”

For example, basic groceries are a need. Premium meal delivery subscriptions are usually a want, not a need. A standard mobile plan might be essential; a high-end upgrade plan may not be.

There’s no judgment here — just clarity.

Step 3: Adjust Gradually

If your housing costs alone exceed 50% of your income — which is common in major UK cities — the rule may need to be adapted.

Rather than drastic cuts, gradual adjustments tend to be more sustainable. The framework is a guide, not a punishment.

Step 4: Review Monthly

Budgets work best when reviewed regularly. Inflation, income changes, and lifestyle shifts all affect the balance.

The goal isn’t perfection. It’s awareness.

A Simple 50/30/20 Budget Example

Imagine your monthly take-home pay is £2,500.

Using the rule:

- 50% Needs: £1,250

- 30% Wants: £750

- 20% Savings/Debt: £500

If your fixed housing and essential bills total £1,300, you’re slightly above the guideline. That doesn’t mean failure — it means the structure may need adjusting, perhaps shifting to 55/25/20 or another realistic split.

Flexibility is key.

Benefits of the 50/30/20 Budget Rule

- Keep It Simple

Many budgeting plans fail because they can be too complicated. When you’re trying to keep track of many categories, it can quickly become confusing. However, by organising your money into just three simple groups, it becomes much easier to understand and follow.

- Built-In Balance

This method helps you find a good balance between having fun with your money today and saving for tomorrow. You don’t have to give up all the enjoyable things in life, and you’re still looking out for your future. This way, you can enjoy what you have now while also setting some aside, making budgeting feel helpful instead of like a limit on your life.

- Makes Saving Automatic

By setting aside 20% of your income from the start, saving becomes part of the routine, not an afterthought. You’re paying yourself first, which keeps your long-term goals front and centre without relying on willpower every month.

4. Keeps Lifestyle Creep in Check

When you start making more money, it can be tempting to spend more as well. Without a budget or plan, that extra cash can vanish in no time. Having a simple approach to managing your money can help you avoid this problem, allowing you to save more rather than just increasing your spending.

Limitations and Real-World Challenges

No budgeting method works perfectly for everyone.

High Housing Costs

In some areas of London and other cities in the UK, people may spend more than half of their take-home pay just on rent or mortgage payments. In these situations, the common rule about how much to spend on housing might not align with what’s actually happening in real life.

Variable Income

People who work independently as freelancers or contractors may find it hard to manage fixed percentages when their income changes from month to month.

Debt Burdens

If there is a lot of debt, reducing it by 20% might not be enough to make a big difference.

Inflation

Rising food and energy costs can push “needs” above 50%, squeezing discretionary and savings categories.

Life Stages

Students, young professionals, families with childcare costs, and those nearing retirement all face different financial pressures.

The 50/30/20 framework is a starting point, not a universal formula.

Is the 50/30/20 Rule Realistic?

For many people early in their financial journey, yes, it provides structure without overwhelm.

However, realism depends heavily on:

- Location

- Income level

- Household size

- Debt obligations

- Cost of living pressures

Some households may operate closer to 60/20/20. Others may prioritise savings at 30% during high-earning years.

The percentages matter less than the intentional allocation of income.

What Counts as “Needs” in 50/30/20?

A common area of confusion is what qualifies as a need.

A helpful test: if you temporarily lost your income, would this expense be unavoidable?

Housing, utilities, food, basic transport — typically yes.

Upgraded streaming bundles or luxury gym memberships — usually no.

Grey areas exist. For example, a car may be essential in rural areas but optional in city centres with public transport. Context matters.

Does the 50/30/20 Rule Include Mortgage Payments?

Yes. Housing costs — whether rent or mortgage — fall under the 50% needs category.

It’s important to include:

- Mortgage repayments

- Council tax

- Essential insurance

- Basic maintenance allowances

Ignoring full housing costs can distort the framework.

What If You Can’t Save 20%?

Many people cannot immediately allocate 20% to savings, especially during cost-of-living pressures. In that case, the principle still holds: prioritise building some surplus, even if smaller. Financial progress is incremental. Consistency often matters more than hitting an exact percentage.

How It Compares to Other Budgeting Methods

50/30/20 vs Zero-Based Budgeting

Zero-based budgeting assigns every pound a specific job. It’s more detailed and hands-on. 50/30/20 is broader and less granular. Those who enjoy detailed tracking may prefer zero-based systems. Those who prefer simplicity may prefer the 50/30/20 approach.

50/30/20 vs 70/20/10 Rule

The 70/20/10 framework allocates:

- 70% to expenses

- 20% to savings

- 10% to debt or giving

The structure is similar but places less emphasis on distinguishing needs from wants. Again, preference depends on personality and financial goals.

The Psychological Benefits of Structured Budgeting

Beyond numbers, budgeting affects behaviour.

Clear allocation:

- Reduces guilt around spending

- Encourages mindful decisions

- Prevents emotional overspending

- Creates visible progress

Behavioural finance research consistently shows that structure improves financial outcomes more reliably than willpower alone. A budget isn’t a restriction. It’s prioritisation.

When the 50/30/20 Rule Works Best

It tends to work well when:

- Income is relatively stable

- Fixed costs are manageable

- You prefer simplicity over detailed tracking

- You are building foundational financial habits

It may require modification when:

- Living costs are unusually high

- Income fluctuates significantly

- Aggressive debt reduction is necessary

- Major life transitions are occurring

Adaptability is a strength, not a weakness.

A Practical Adjustment Framework

If you’re evaluating whether this method suits you, consider:

- What percentage of income is currently fixed?

- Do you have adequate emergency liquidity?

- Are you comfortable with your current savings rate?

- Are debts accumulating interest faster than savings grow?

- How stable is your income over the next 3–5 years?

Thinking in this structured way is often more valuable than following exact ratios.

The Broader Principle Behind 50/30/20 Budgeting Rule

The important lesson here is not just about the numbers. It’s about these ideas:

– When you spend money, do it on purpose.

– Save money regularly.

– Make lifestyle choices that match your long-term goals.

Finding financial stability usually doesn’t happen from one big decision. It usually comes from small, steady habits that you keep for a long time.

Related articles:

How To Build An Emergency Fund

Final Thoughts

The easiest 50/30/20 budgeting rule guide isn’t about rigid percentages. It’s about awareness, which helps you feel more in control of your financial situation.

It encourages you to see clearly where your money goes, to balance present enjoyment with future security, and to create a structure that reduces financial stress rather than increasing it.

For some, the exact 50/30/20 split will work well. For others, adjustments will be necessary. That’s perfectly normal.

The real value lies in consistently applying a thoughtful framework, reviewing it as circumstances change, and aligning your financial structure with your stage of life.

When it comes to making financial choices, things can get complicated, especially if you have a lot of money, need to think about taxes, or are planning for the future. Getting help from a qualified financial expert can give you clear advice that fits your situation.

Remember, budgeting isn’t just about cutting back on spending. It’s about control — steady, thoughtful control over where your money flows and how it supports the life you’re building.

How to Start Investing for Beginners (Starting With Just £10)

Leave a Reply