What Is an Emergency Fund?

If you’ve ever had your car break down the same week your rent or mortgage was due, you already understand—emotionally, if not financially—why an building an emergency fund matters. At its core, an emergency fund is a dedicated pool of cash reserves set aside specifically for unexpected expenses. Think job loss, medical bills, urgent home repairs, or that refrigerator that decides retirement sounds better than chilling your groceries. This isn’t money for vacations or flash sales—it’s your personal financial airbag.

According to UK financial surveys, many households would struggle to cover even a £300–£500 unexpected expense with readily accessible cash. This shows why it’s important to have some cash saved for emergencies. It helps keep your finances strong over time. If you don’t have money saved, even a small expense, like a car repair, fixing your home, or a sudden medical bill, can turn into big debt through overdrafts, credit cards, or loans.

This shows why having a cash emergency fund is very important—it is a key part of having long-term financial security. Without money available, even a small problem can turn into big debts, like high-interest credit card bills or personal loans.

Keeping your emergency fund in an FSCS-protected savings account ensures your money is safe and easily accessible when needed. Using careful budgeting and automatic savings transfers can help you save money over time. This makes it easier to create a financial cushion, so you don’t have to worry about small problems affecting your money. In simple words, an emergency fund is not just a backup; it is a smart way to achieve stability, independence, and peace of mind.

An emergency fund also supports your long-term financial strategy by preserving your investments. When markets dip or inflation rises, you don’t want to liquidate retirement accounts prematurely. Liquidity—the ability to access money quickly without penalties—is what makes an emergency fund powerful. It’s not about growing wealth; it’s about protecting it.

How to build an emergency fund: a step-by-step guide

- Set a starter goal – Begin with a small, achievable target like £500–£1,000 to cover minor unexpected expenses.

- Calculate essential expenses – Review your household budget and tally fixed and variable costs to determine your three- to six-month target.

- Choose the right account – Keep your fund in a safe, accessible savings account or easy-access high-yield savings account for liquidity and protection.

- Automate contributions – Use automatic transfers or direct deposit allocations to build consistency.

- Track and adjust – Use budgeting apps to monitor progress and increase contributions as income allows.

- Replenish after use – Every time you withdraw funds for an emergency, restore them to maintain your financial buffer.

Emergency Fund: Your First Line of Financial Defence

An emergency fund is a dedicated savings account you set up for unplanned expenditures. Its main purpose is to help you stay financially stable when something surprising happens, like a huge car repair or an unexpected medical bill you have not planned for.

Because life can be unpredictable, having money saved in an emergency fund helps you handle these situations without extra worry. This savings acts like a safety net, making sure you can meet urgent money needs and feel more secure about your finances.

Unlike investment accounts, which can change in value, an emergency fund is meant to stay stable and safe. Organisations like the Consumer Financial Protection Bureau suggest having easy-to-access emergency savings is the key. This is important. You’re not saving to make money; you’re saving to be ready when things get tough.

Why is this so critical? Because risk is not theoretical—it’s statistical. Job transitions, health issues, and sudden repairs are normal life events. Without a savings buffer, many people resort to high-interest debt products. And once you’re paying 20%+ interest on a credit card, your financial progress slows dramatically.

A well-funded emergency account gives you control, confidence, and breathing space. It lets you make rational decisions instead of desperate ones, protecting your credit score, your peace of mind, and your financial momentum. In short, your emergency fund

Emergency Fund vs General Savings: Know the Difference

It’s important to clear up a common misconception: an emergency fund is not the same as general savings. While both involve putting money aside, their purpose—and mindset—are entirely different.

General savings cover holidays, gifts, or a future home renovation. An emergency fund, however, is reserved exclusively for genuine financial emergencies. Using it for non-essential expenses weakens its protective role. Think of it as self-funded insurance: its sole job is to shield you from unexpected financial shocks.

Having your money safe and easy to access is much more important than trying to earn high returns. In the UK, deposits in eligible banks are protected up to £85,000 by the Financial Services Compensation Scheme (FSCS). It’s important to keep your emergency savings in a safe, easy-to-access account rather than risky investments.

Accessibility without temptation is key. Your emergency fund should be separate from your everyday current account to reduce the risk of impulse withdrawals. Having a separate account helps you manage your money better and keeps your financial safety net safe.

By clearly defining boundaries—“emergency money” versus “lifestyle money”—you create structure, resilience, and long-term security in your financial plan.

Why Liquidity Matters During Economic Hard Times

A common misconception amongst a lot of people is that having assets like stocks or real estate indicates one has money on hand. Although these assets have the potential to increase wealth over time, they do not offer readily accessible funds. Making wise financial decisions and effectively managing your finances depend on your understanding of this distinction.

Cash, whether in a bank account or savings, is what allows you to cover unexpected expenses straight away, whereas other investments may take time to access or sell.

Assets can help you feel secure in the long run and can increase in value, but they often can’t be turned into cash quickly. For example, selling your house or withdrawing money from a retirement account can take time and might not yield the best price if the market changes.

On the other hand, having cash available means you can pay for urgent needs or take advantage of good opportunities right away. Understanding the difference between assets and cash is very important for making smart financial choices.

It helps you keep a good mix between growing your money with investments and having enough cash for daily needs and surprises. Knowing this is important for smart money planning and being ready for emergencies. When times are hard, it’s really important to be able to get cash quickly without losing money because of penalties or market drops.

Economic problems and high prices can seriously impact the value of your investments. If you need to sell your investments during a downturn, you may have to sell them for less than what you paid. This is why having an emergency fund is essential. An emergency fund lets you handle urgent expenses without touching your long-term investments.

A good emergency fund often starts at a specific amount—usually about £1,000—to help with small financial issues. Financial experts recommend building this fund to cover three to six months’ worth of living expenses. This way, you can take care of important bills like housing, utilities, insurance, and food if you suddenly lose your income.

Having money available when you need it is very important. It means you have choices when you want to change jobs, and it helps you deal with life changes. It can also make tough times, like economic problems, a little easier. Having a good amount of savings can reduce stress and help you feel more secure. This peace of mind is worth more than just having money.

Why You Need an Emergency Fund?

Life can be surprising and costly, for example, getting a flat tyre can happen at any time, and it doesn’t matter how much money you have. Also, if your job changes suddenly, you can’t wait for your next paycheck to deal with it. And a surprise medical bill certainly doesn’t ask if this is a convenient time.

The importance of emergency savings lies in one powerful outcome: debt avoidance. When a short-term crisis hits, your emergency money steps in before high-interest borrowing does. Without it, many people turn to credit cards, personal loans, or even early withdrawals from retirement accounts. That decision, often made under pressure, can create long-term financial consequences that outlast the original emergency.

According to data published by the Office Of National Statistics in recent economic well-being reports, many adults would struggle to cover even modest emergency expenses without borrowing. 4 in 10 adults did not expect to save any money in the coming year in early 2023. That statistic isn’t meant to alarm you—it’s meant to clarify the stakes. An emergency fund isn’t about pessimism; it’s about financial preparedness. It’s about planning calmly so you don’t panic later.

Protection Against Job Loss and Income Disruption

Let’s discuss something that can lead to big money problems: losing a job. The job market can change fast because of reasons like a bad economy, changes in a company, or new technology. Even the most skilled workers can be let go. When someone loses their job, their bills and expenses don’t stop just because they no longer have an income.

Unemployment benefits can help for a short time, but they often do not pay enough to cover what you used to earn and can take time to get started. Meanwhile, you still need to pay for things like rent, utilities, groceries, and insurance. These obligations continue regardless of whether or not you have a job.

Having an emergency fund is very important. It is like a safety net to help you when things go wrong. This money can help you pay for essentials while you are without work, reducing your financial stress. It gives you the time you need to find a job that is right for you, rather than feeling forced to take the first job you see.Having an emergency fund is a smart way to manage risk. While you can’t completely prevent job loss, you can prepare financially for it. An emergency fund can turn losing a job from a disaster into a situation you can handle.

Medical Emergencies and the Gaps That Insurance Doesn’t Cover

Even with good NHS services or private health insurance, you can still face unexpected medical costs. This includes things like prescription charges, dental and eye care, planned surgeries, and private treatments. A brief stay in the hospital, urgent dental care, or sudden surgery can lead to high expenses that you have to pay yourself.

Medical issues also can create a double whammy: costs rise while your income may fall if you’re unable to work temporarily. Your household budget then feels pressure from both sides—a classic short-term crisis scenario.

Many families use high-interest loans, such as credit cards or overdrafts, when they don’t have an emergency fund. Even small medical bills can quickly add up and cause big money problems. This isn’t meant to scare you; it just shows how quickly health costs can add up if you’re not ready for them.

Maintaining your health is crucial, and having a good emergency fund set aside for medical emergencies can help. You won’t have to worry about money if you have emergency funds saved. Everyone should think about making this sensible choice.

Car Repairs, Home Repairs, and Everyday Financial Reality

Let’s discuss some everyday problems that can still cause a lot of trouble. These include things like your car breaking down, your heating system breaking when it’s cold outside, or a water leak happening right before you have to pay your bills. These events are common in life. They don’t happen rarely; instead, they happen often when you least expect them.

When these repairs arise, people without savings often turn to high-interest borrowing, adding to their existing Credit card debt. The problem? Credit card interest compounds quickly. A £2,000 repair can cost far more if it’s paid off slowly at 20% or even 34% interest with some credit card companies.

This is where the practical side of why to save for emergencies becomes crystal clear. Having emergency savings can turn an unexpected cost into a minor problem rather than a serious financial issue. It helps protect your future goals from unexpected events.

Avoiding debt isn’t just about discipline; it’s about structure. A properly funded emergency account supports debt avoidance, stabilises your cash flow, and preserves your credit score. It keeps one unexpected repair from becoming years of repayment.

The Psychological Impact: Reducing Financial Stress

There is something very important beyond numbers and charts: having peace of mind. When money problems occur, they can cause a lot of stress. This stress can make it hard to sleep, do your work well, get along with others, and even stay healthy. Money worries don’t stop when the workday ends.

An emergency fund changes your mindset. Instead of thinking, “What if something goes wrong?” you think, “If something goes wrong, I’m covered.” That subtle shift is powerful. It strengthens decision-making, reduces anxiety, and improves overall well-being. The importance of emergency savings is not just mathematical—it’s emotional and strategic. It’s about creating stability in an unstable world. When you build emergency savings, you’re not expecting disaster. You’re preparing intelligently. And in personal finance, preparation always outperforms panic.

The Ultimate Guide to Saving Money Without Feeling Restricted

How Much Should You Save?

Now we come to a common question: How much money should we save for emergencies? The clear and straightforward answer is that it depends on you. A common guideline is to save enough money to cover three to six months of your basic living expenses. However, this is just a starting point and not the same for everyone.

Financial planners usually recommend saving enough money for “3–6 months” of expenses. This means that if you lose your job or face an emergency, three months of savings can help you get through a short period without income. Saving for six months is even better because it gives you more security in case recovery takes longer. The best amount to save depends on how stable your income is, whether you have people depending on you, and the level of risk you face.

According to research by the Financial Conduct Authority’s (FCA) Financial Lives survey, one in 10 Britons has no savings to cover even one month of their expenses. This shows why having a clear savings goal is important. If you don’t have a specific amount in mind, it can feel confusing. But when you have a clear number, it is easier to see what you need to do to reach your goal.

Let’s look at this practically, because having clear goals can help you feel more confident.

Step One — Calculate Your True Monthly Expenses

Before you decide whether you need three months or six, you must calculate your baseline monthly expenses accurately. And this is where precision matters. We’re not calculating lifestyle luxuries—we’re identifying essential spending.

Start with your household budget and separate expenses into two categories: fixed expenses and variable costs. Rent or house rent, utility bills (such as water and electricity), insurance, loan payments, and groceries (food and household goods) are examples of fixed expenses—bills that don’t vary significantly each month. Expenses that are subject to change include transportation, household supplies, and gas for your vehicle. These expenses may increase or decrease, but they must still be covered.

Do not include discretionary spending like vacations, streaming upgrades, or dining out frequently. In an emergency scenario, those can be trimmed. Your emergency fund protects survival, not convenience.

For example, if your essential monthly expenses total £3,000, your 3 month savings rule target would be £9,000. A full 6 month savings cushion would be £18,000. Here is your personal emergency fund calculator: take your monthly essential expenses and multiply that by the number of months you’d like to have covered.

Emergency Fund Calculator (UK Example)

Step 1: Calculate Your Essential Monthly Expenses

Include only necessary spending such as:

- Rent/mortgage: £________

- Utilities (gas, electricity, water, broadband): £________

- Council tax: £________

- Groceries: £________

- Insurance (home, health, car): £________

- Transport costs (fuel, public transport): £________

- Loan repayments: £________

- Total Monthly Essentials = £________

Step 2: Decide How Many Months to Cover

- 3 months – Single with stable income

- 6 months – Families or variable income

- 9 months – Self-employed or high-risk jobs

Number of Months = _______

Step 3: Calculate Your Target Emergency Fund

Target Emergency Fund = Total Monthly Essentials × Number of Months

Example:

- Monthly essentials = £2,000

- Coverage = 6 months

- Target emergency fund = £2,000 × 6 = £12,000

Step 4: Plan Your Savings

- Starter goal: £200–£1,000

- Monthly contribution: £________

- Time to reach full fund = Target Emergency Fund ÷ Monthly Contribution

Example:

- Target = £12,000

- Monthly contribution = £300

- Time to reach goal = 12,000 ÷ 300 = 40 months (3 years 4 months)

Clarity transforms overwhelm into structure. Once you know your number, you’re no longer guessing—you’re building intentionally.

Single vs Family Households

Your living situation affects how much money you should keep saved for emergencies. If you are single and don’t have many bills to pay, saving enough for about three months’ worth of essential costs might be enough. It’s easier for you to manage a simple budget and deal with unexpected expenses.

If you support a partner, children, or other dependents, your margin for error shrinks. More people in your household mean higher essential spending, additional healthcare costs, and greater exposure to financial disruption. In these cases, aiming for a six-month buffer—or more—provides extra security.

Families can face many risks all at once. If someone gets sick, changes jobs, or has to move suddenly, it can affect many family members together. Because of this, it’s important to have enough emergency support to handle these extra challenges.

Location also matters. Living in London, Manchester, Edinburgh, or other high-cost urban areas typically means higher rent, transport, and daily living costs than in smaller towns or rural regions. For example, essential monthly expenses of £3,500 in London might only be £2,000 elsewhere. Your emergency fund should reflect your own household reality, not a national average.

Self-Employed, Freelancers, and High-Risk Careers

If you work for yourself as a Freelancer or in the gig economy, you need to change your plan. Freelancers, contractors, and professionals who work on commission often have income streams that change. Even people who do well at work can have slow periods or late payments.

Lower income stability increases financial volatility. For this reason, many financial advisors recommend that self-employed individuals hold six to nine months of essential expenses in reserve. This extended cushion protects against contract gaps and client turnover.

Similarly, individuals working in high-risk industries—such as construction, sales, startups, or cyclical sectors—may face higher layoff probabilities during economic downturns. If your job changes a lot because of the market, your emergency fund should be enough to help with that uncertainty.

This isn’t pessimism; it’s strategy. Risk exposure and savings levels should align. The greater the variability in your income, the stronger your financial foundation must be.

Setting a Realistic Savings Goal Without Overwhelm

If the numbers seem daunting at the moment. It can be discouraging to consider a large savings target, such as £10,000. However, emergency funds are actually developed gradually rather than all at once.

Start with a starter emergency fund milestone—often £1,000. That covers minor disruptions, such as car repairs or medical deductibles. Once that is secured, gradually build toward three months. Then reassess whether six months makes sense for your situation.

The key question isn’t just how much emergency fund you need. It’s: what level of protection allows you to sleep well at night?

AQs a reminder, financial confidence grows through measurable progress:

- Find your goal number.

- Divide it into smaller steps.

- Set up automatic payments to save regularly.

- Check your progress every three months.

- Change your plan as your household expenses change.

Your emergency fund isn’t about predicting disaster—it’s about engineering stability. And stability, in personal finance, is the platform on which wealth is built.

Where Should You Keep Your Emergency Fund?

Once you’ve worked out your savings target, the next logical question is practical: what’s the best place for an emergency fund? The answer revolves around three non-negotiables—liquidity, safety, and accessibility. Your emergency savings are not there to perform acrobatics in the stock market. They are there to sit quietly, remain available, and protect you when life throws a financial curveball.

Your top priority should be capital preservation and immediate access to withdrawals. That means choosing a safe savings account with minimal risk and protected deposits. Unlike long-term investments, your emergency fund should not fluctuate in value. If the stock market goes down the same week your boiler stops working, you want to feel safe and secure, not worried and stressed.

When interest rates change often, many people are tempted to pursue larger returns. Emergency funds are mainly for keeping your money safe rather than earning a lot of interest. The best place for your emergency fund is a very reliable savings account that can also earn a little interest. Focus on keeping your money safe instead of hoping for big gains.

High-Yield (Easy-Access) Savings Accounts — The Practical Choice

An easy-access savings account offered by traditional institutions or online banks can be an excellent emergency savings account that pays good interest rates and lets you access your money quickly, with no fees. If your car unexpectedly fails its MOT, you shouldn’t have to wait a long time or pay extra to get your money back.

The main benefits of these accounts are easy access to your money and steady returns. Although interest rates may change, these accounts help your savings grow over time. Even a small increase can help you keep your buying power, which is important, especially with inflation, and you don’t have to take extra risks.

It’s important to keep your savings safe. In the UK, the Financial Services Compensation Scheme (FSCS) keeps your money safe. If the bank or financial service has a problem, they protect your money up to a certain limit. The idea is the same: you should keep your emergency money in a bank or financial institution that is backed by the government to ensure its safety.

If you’re asking, where to store emergency savings safely? — An easy-access, protected account is typically your strongest starting point.

Why You Should Avoid Investing Your Emergency Fund

Let’s clear up a common misunderstanding: putting your emergency money into investments is riskier than it is smart. Indeed, markets generally rise over the long term. However, emergencies can happen quickly and shouldn’t be put off for the long run.

Investing in stocks, funds, or property exposes your safety net to volatility. If markets dip 15% and you need funds immediately, you are forced to sell at a loss. That undermines the entire purpose of capital preservation.

Even during periods of rising interest rates, the temptation to seek higher returns through investments can blur judgment. But your emergency fund has one job: be available and intact. Separate your wealth-building strategy from your risk-management strategy. Investments build growth. Emergency funds provide stability. Mixing the two increases vulnerability.

The Golden Rules for Choosing the Best Place for Your Emergency Fund

To summarise, the best place for emergency fund storage in the UK should meet five criteria:

- Fully protected deposits (via UK compensation schemes)

- Immediate withdrawal access

- Competitive but stable interest

- No penalties for access

- Clear separation from daily spending accounts

In short, you’re looking for a safe savings account that balances security with modest growth. Whether through established banks or reputable online banks, the goal remains the same: keep your emergency savings accessible, protected, and untouched unless genuinely needed.

Because when an emergency happens—and eventually, one will—you don’t want to be asking where your money is. You want to know exactly where it sits, ready to do its job.

How to Start Building Your Emergency Fund

Step One — Set Small, Achievable Milestones

When people try to save money quickly, they often hurt their own efforts by setting goals that are too big, too soon. If your final aim is to save £9,000, that amount can feel scary. Instead, begin with a simple savings plan that is easy to follow.

Start by choosing a small goal, such as saving £500. Then, aim for £1,000. Next, try to save enough for one month of basic costs. Breaking your big goal into smaller steps helps you feel good when you achieve them. Each time you reach a goal, it makes you feel more confident and motivated to keep going.

This isn’t just an idea—it’s about how people think about money. We are more motivated by seeing progress right away rather than thinking about something far away. Think of your emergency fund like a staircase that you climb step by step, not like a tall cliff that feels too hard to reach.

The first step is to figure out how much you can save each month that fits your budget. Even if you save just £100 every month, that adds up to £1,200 in a year. If you include a little extra money, like bonuses, tax refunds, or money from freelance work, you can save even faster. The goal isn’t speed alone—it’s sustainability. Small, steady deposits outperform inconsistent bursts of enthusiasm.

Cut Discretionary Spending Without Feeling Deprived

The phrase “cut expenses” can sound like you’re losing something important. But if you look carefully at your spending, you might find that small changes can help you save money without making big sacrifices.

Start by looking at your recent bank statements. Find areas where you are spending too much money on things that don’t add much value, like subscriptions you don’t use, impulse buys online, and takeout meals that aren’t worth the price. If you can save just £50–£100 each month and put it into your emergency fund, it can really help it grow.

The goal is to make smart decisions rather than feel deprived. You should switch from premium subscriptions to regular plans, cut down on takeout meals, and see if you can get better deals on your services. These small changes can add up over time and help you save a lot.

If you want to save money quickly, focus on this for the next 3 months. Try to cut back on non-essential spending and save the extra money you have for your emergency fund. This focused effort can help you build your financial safety net.

Getting to a place of financial security doesn’t mean you have to be very frugal or give up everything you enjoy. It’s more about being aware of your spending and taking consistent, smart actions. This is what leads to real results in your finances.

How to Stop Living Paycheck-to-Paycheck (A Beginner Action Plan)

Automate Everything — Remove Emotion from the Equation

If you rely on willpower to save, you will eventually lose convenience. The most effective emergency fund tips always include one principle: automate your savings.

Set up automatic transfers from your current account into your dedicated savings account immediately after payday. This technique—often referred to as “pay yourself first”—ensures saving happens before discretionary spending.

If your job lets you split your paycheck with direct deposit, you can send part of your pay straight into your savings to remove temptation entirely. You won’t miss what you never see.

This is called savings automation, and it transforms financial goals into background processes. Instead of deciding each month whether you’ll save, the decision has already been made.

Many modern budgeting apps also let you set savings goals, track progress, and automatically categorise spending. Visibility strengthens accountability. And accountability strengthens habits.

Automation isn’t about rigidity—it’s about removing friction. The less effort required, the more consistent your progress.

Use the 50/30/20 Rule as a Practical Framework

If you’re looking for a simple budgeting structure, the 50/30/20 rule provides clarity. This method divides your income into three categories:

- 50% for needs** (such as rent, utilities, groceries, and insurance)

- 30% for wants** (like dining out, subscriptions, and leisure activities)

- 20% for savings and debt repayment**

When it comes to the 20%, prioritise building your emergency fund first until it reaches your desired amount.

Keep in mind that this framework isn’t a strict rule. If you live in a high-cost-of-living area, your “needs” may exceed 50%, so feel free to adjust your allocations accordingly. The goal is to create a structured plan rather than to pursue perfection.

By consistently setting aside a portion of your income for savings, you cultivate disciplined progress. This approach converts abstract goals into measurable actions.

The best part? Once your emergency fund is fully funded, you can redirect that same 20% toward investing and wealth-building. You’re not just creating a financial cushion; you’re also gaining financial momentum.

Related articles:

How To Build An Emergency Fund

Saving Money Without Feeling Restricted

How To Stop Living Paycheck-To-Paycheck

Conclusion: Build the Habit First, Grow the Balance Second

Real financial success isn’t just about how much money you have saved. It’s more about the system you create to manage your money. Building an Emergency Fund by using a simple budget, setting up automatic savings, and setting clear financial goals, you can build strong money habits that last.

An emergency fund is created by regularly saving money. Regular saving helps you learn to manage your money better, which can lead to building wealth over time.

If you want to save money faster, start with small amounts you can manage. Set up automatic savings so the money goes into your savings account without you having to think about it. Keep track of your savings with helpful tools and online apps, and change your plan if needed. At first, it may feel like you’re not saving much, but over time, the money will grow because of interest.

When unexpected expenses come up, you can handle them confidently—not by luck, but because you have planned and prepared for these situations.

The true importance of an emergency fund goes beyond just having money. It brings you peace of mind. When you have easy access to cash, keep it safe, and regularly add to it, you build a strong foundation for other financial goals. This can include paying off debts, saving for retirement, or investing. An emergency fund is not only about having money saved. It’s a way to help you when unexpected things happen; it symbolises freedom, safety, and confidence in a world that can sometimes be uncertain.

FAQ’s

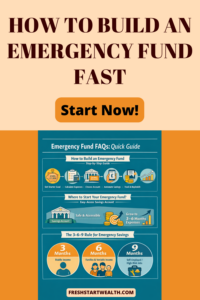

Where should I start my emergency fund?

Start by opening a dedicated easy-access savings account separate from your everyday current account. This keeps your emergency money safe, liquid, and clearly earmarked for true emergencies only. Begin with a starter emergency fund of £500–£1,000, and gradually grow it toward three to six months of essential expenses.

What is the 3-6-9 rule for emergency funds?

The 3-6-9 rule is a flexible approach to setting your emergency fund target based on risk and household circumstances:

- 3 months of essential expenses – suitable for single individuals with stable income.

- 6 months – recommended for families or those with variable income.

- 9 months – ideal for self-employed people, freelancers, or those in high-risk jobs.

This framework balances liquidity with realistic financial preparedness.

How do you start your emergency fund?

To start, set a small, achievable goal (£500–£1,000) in a dedicated savings account. Automate contributions from your income using automatic transfers or direct deposit, and cut non-essential spending to accelerate progress. Track your monthly allocations and increase contributions incrementally until you reach your full three- to six-month target.

Leave a Reply