How to Pay Off Debt

Debt has a unique way of taking up space in your head.

It’s there when you wake up.

It hums quietly in the background during the day.

And it shows up loudly at night, when the world goes quiet, and your thoughts get loud.

For many people, debt isn’t just numbers on a screen or on paper. It’s a shame. It’s fear. It’s a constant sense of being behind. It’s the feeling that no matter how hard you try, you’re always starting from a deficit.

And the advice people give doesn’t help.

“Just pay it off faster.”

“Cut everything.”

“Stop spending.”

“Work more.”

None of that addresses the emotional weight of debt — or the reality of living an authentic life while trying to escape it.

This guide is different. This is not about extremes, punishment, or living like a hermit. This is about paying off debt in a calm, realistic, and sustainable way, without burning out or giving up halfway through.

You don’t need more pressure.

You need a plan that works with you.

Why Debt Feels So Overwhelming (Even When the Numbers Aren’t Huge)

One of the most important things to understand about debt is this:

- The stress of debt is often psychological before it’s mathematical.

Two people can owe the same amount, but experience it completely differently. One feels calm and in control. The other feels trapped and panicked.

Why?

Debt can feel overwhelming when:

– We don’t have a clear plan for how to handle it.

– We don’t know when it will be over.

– We feel judged by others or even by ourselves.

– We think our debt says something negative about who we are.

Debt can lead to a lot of mental clutter. Every bill, every statement, and every minimum payment serves as a reminder that something isn’t settled. Our minds dislike things that are unresolved.

Before we talk about ways to manage debt or the numbers involved, let’s remember something very important:

– You are not bad with money.

– You are not broken.

– You are not failing.

You are dealing with a complex, emotional system that is rarely taught well. And that means this can be learned, and changed.

The Biggest Debt Mistake: Trying to Fix Everything at Once

When people finally decide to face their debt, they often swing to the opposite extreme.

They want it gone now.

So they:

- Try to pay off all debts at once

- Cut every comfort

- Live on unrealistic budgets.

- Use pure willpower

- Expect immediate progress

And when life pushes back — as it always does — they feel defeated and quit.

Here’s the truth most people miss:

- Debt freedom is not built through intensity. It’s built through consistency.

The goal is not to suffer through debt payoff. The goal is to outlast it.

That means choosing a strategy you can maintain even on tired, stressful, imperfect days.

Step 1: Face the Numbers (Without Judgement)

Managing debt can be very difficult at times, but if you ignore it, things can get worse later on. It’s essential to address it. To manage your debt better, it’s vital to get the correct information and take your time when making decisions.

First, write down important details about each of your debts, such as:

– How much money you owe in total.

– Your current balance (the amount you still need to pay).

– The interest rate (the extra cost you pay on your debt) for each one.

– The minimum payment required each month.

This organised approach will help you gain a clearer understanding of your financial situation and create a plan for managing your obligations.

Do this without letting your feelings get in the way, and focus on the facts.

You might find one of these two thoughts surprising:

- “It’s not as scary as I thought.”

- “Now I know exactly what I’m dealing with.”

Both of these thoughts are good. When you understand your debt better, it becomes much easier to plan and manage it.

Step 2: Stop the Bleeding Before You Start Paying Aggressively

This step is critical — and often skipped.

Before you focus on paying off debt, you must prevent new debt from forming.

That means:

- Building a small emergency fund (£500–£1,000)

- Getting current on minimum payments

- Creating a basic working budget

- Pausing unnecessary credit use

Why?

Because paying off debt while constantly adding to it is like trying to drain a bath with the tap still running.

Stability first. Speed later.

Step 3: Choose a Debt Payoff Method That Fits Your Brain

There is no “best” debt payoff method — only the one you’ll stick with.

The two most effective approaches:

The Debt Snowball vs Debt Avalanche methods

Here’s a graph illustrating the Debt Snowball vs Debt Avalanche methods for paying off debt.

1. The Debt Snowball (Best for Motivation)

You pay off your debts starting with the smallest, then move on to the next-largest, and continue this way. It doesn’t matter what the interest rates are.

Why it works:

- Quick wins build confidence

- Keeping your movement helps you continue.

- Seeing progress makes you feel good.

This way of paying off your debt is very effective if dealing with debt feels emotionally challenging. It’s not just numbers on a screen or on paper.

2. The Debt Avalanche (Best for Saving Money)

You pay off debts from the highest interest rate to the lowest.

Why it works:

- You pay less interest overall

- It’s mathematically efficient

This method is powerful if you’re motivated by logic and long-term savings.

Which One Should You Choose?

Ask yourself:

- Do I need motivation? → Snowball

- Do I want maximum efficiency? → Avalanche

Both work. Neither is wrong. The only bad method is the one you abandon.

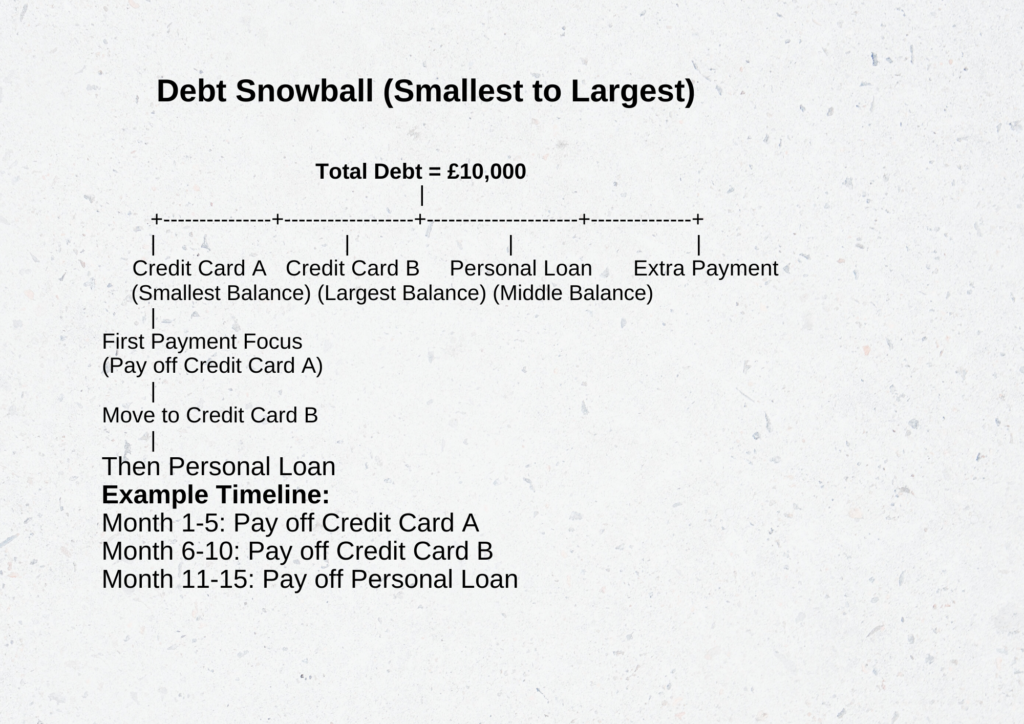

Debt Snowball Method:

- Focus: Start by paying off your smallest debts first. It doesn’t matter what the interest rates are. After you fully pay off one debt, move on to the next smallest one.

- Psychological Benefit: Gives a sense of accomplishment as smaller debts are eliminated first, building momentum.

How it works:

- List your debts from smallest to largest.

- Make the minimum payments on all your debts. Use any extra money to pay off the smallest debt first.

- Once the smallest debt is paid off, move to the next smallest, and so on.

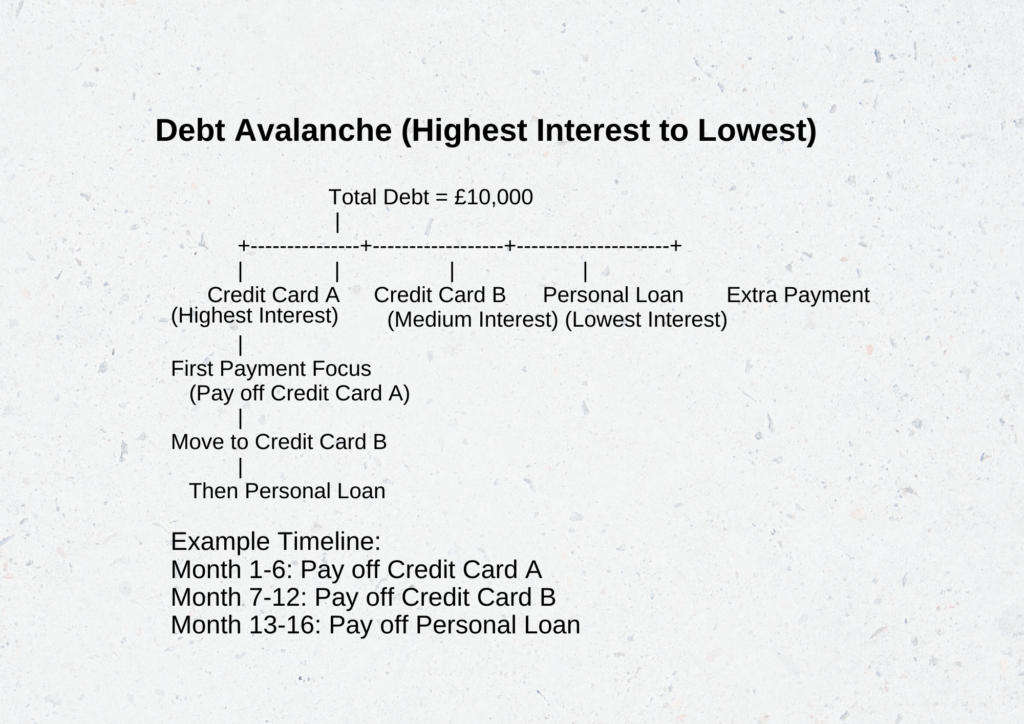

Debt Avalanche Method:

- Focus: Pay off the highest-interest debt first, regardless of the balance. Once that’s paid off, move on to the next-highest-interest debt.

- Psychological Benefit: Saves more money in the long term, but may not feel as rewarding early on.

How it works:

- Write down your debts, starting with the one with the highest interest rate and working down to the one with the lowest.

- Pay the least amount on all your debts, but use any extra money to pay off the debt that has the highest interest rate first.

- Once the highest-interest debt is paid off, move to the next highest, and so on.

Debt Snowball vs. Debt Avalanche – Example Modular Graph

Assumptions for Example:

- Total Debt: £10,000

- Minimum Payments: £300/month (combined for all debts)

- Extra Payment: £200/month towards debt payoff

Debt Breakdown:

| Debt Type | Balance (£) | Interest Rate (%) | Minimum Payment (£) |

| Credit Card A | £2,500 | 18% | £50 |

| Credit Card B | £4,000 | 12% | £60 |

| Personal Loan | £3,500 | 7% | £80 |

How it works

For the Debt Snowball method, the smallest balance (Credit Card A) gets paid off first, then moves to the next smallest (Credit Card B), and finally the personal loan.

For the Debt Avalanche method, the highest interest rate (Credit Card A) gets paid off first, then the next highest (Credit Card B), and lastly the personal loan (lowest interest).

Step 4: Create Your “Minimum + 1” Strategy

This plan helps you feel less overwhelmed when managing your debts. Instead of trying to change all your financial issues at once, follow this simple method:

- Make the minimum payments on all your debts.

- Choose one specific debt to focus on.

- Use any extra money to pay off that one debt.

Even paying an extra £20 can be helpful.

Why this method works:

– Simple to Understand: It’s easier to focus on just one debt at a time.

– Fewer Choices: Fewer options help you make decisions more quickly.

– Track Your Success: Paying off one debt shows your progress clearly.

– Less Worry: Focusing on one thing lowers your money stress.

Once you pay off the chosen debt, apply the amount you were paying to the next debt. This way, you keep reducing your debts step by step to help you build momentum and keep going.

Step 5: Find Extra Debt Money Without Punishing Yourself

Many people believe that paying off debt means giving up a lot of things and making big sacrifices. But there are other ways to handle debt that don’t need such big changes to your life. Here are some simple ideas:

– Look at your subscriptions and cancel the ones you don’t use.

– Cut back a little in certain spending areas.

– Use bonuses or tax refunds to pay down debt.

– Sell things you don’t use or need anymore.

– Try short-term money challenges instead of being frugal all the time.

It’s important to know that you don’t have to give up fun or happiness to get out of debt. Instead, you can make smart choices about your money. The best ways to manage debt are those that let you enjoy life while still working towards your financial goals.

How to Stop Living Paycheck-to-Paycheck (A Beginner Action Plan)

Step 6: Automate What You Can (Remove Emotion)

Managing debt can be easier if you make it less stressful. Automated systems are a great way to help. Here’s how to set it up:

- Automatic Minimum Payments: Set up automatic bank transfers to pay the minimum amount on all your debts, which ensures you pay on time and avoid extra fees.

- Automatic Extra Payments: Choose to automatically send extra money to pay off certain debts, like those with high interest rates, to help you pay them off faster and save on interest.

- Due Date Alerts: Use reminders or notifications on your phone or computer to let you know when payments are due, which helps you manage your bills better.

Benefits of Automation:

– Avoid Missing Payments: Using automatic payments can help you remember when to pay bills, so you don’t forget and stay in good financial shape.

– Protect Your Credit Score: It’s very important to pay your bills on time to help you avoid extra fees and keep your credit score in good standing. When you pay your bills on time, it shows that you are responsible with money. This can help you manage your finances better.

– Less Stress: When you set up automatic payments, you don’t have to worry as much about your bills and debts. This helps you feel calmer and gives you more time to think about other essential things in your life.

– Steady Progress: With automation, paying off debt becomes easier and more organised, helping you move closer to financial freedom.

Using these automated systems can help you manage your debt more effectively. This way, you can focus more on planning your money and less on stressing about payments.

Step 7: Expect Boring Months (They Matter More Than Big Wins)

Paying off debt is not always fun like it is in the movies, but it has its benefits. It usually looks like this:

– Doing small tasks every day

– Doing the same things over and over

– Moving slowly towards your goal

– Starting off slowly

This is completely normal. It might feel boring to spend a lot of time doing these things, but it is not a failure. It is an important part of handling your debt in a good way.

The real danger is giving up on your plan during these quiet times, especially when it feels like nothing is changing. In truth, important things are happening:

– Your debt is getting smaller.

– The impact of interest is going down.

– You are getting better at managing your money.

Knowing this is important to help you stay motivated and committed as you work to pay off your debt.

What to Do When Motivation Drops (Because It Will)

Motivation can come and go, but systems last a long time. When you feel less motivated, try these tips:

- Look at how far you’ve come—check the important goals you’ve reached.

- Think about the problems or challenges you’ve managed to solve.

- Remember why you started your journey in the first place.

- Focus on being steady in your efforts instead of how fast you move forward.

- Understand that you don’t need to feel inspired all the time to keep going.

The important thing is to keep making progress, even when you don’t feel very motivated.

Should You Use Windfalls to Pay Off Debt?

Yes — but thoughtfully. This is not a financial advice, it’s an educational.

When you get extra money that you didn’t expect, it can be a good chance to help with your money problems. Using this money wisely can help you pay off debt and feel safer about your finances in the future. You might get extra money from different sources:

– Tax Refunds: A lot of people are excited for tax season because it’s a time when they can get back money they paid too much during the year. A tax refund can give you extra cash, which you can use to pay off debts. Think about using some or all of your refund money to pay off debts that have high interest, like credit cards or personal loans.

– Work Bonuses: You might receive bonuses at work for good performance. Instead of spending this money on fun things, think about using a big part of it to pay off your debts. This can help decrease the amount you owe and lower the interest you’ll pay in the future.

– Gifts from Family or Friends: Occasionally, family or friends may give you money as a gift. It can be tempting to spend it right away, but using this money to reduce your debts can significantly improve your financial situation and lower your stress.

– Other Unexpected Money: Life can surprise you with unexpected money, like an inheritance, winning a prize, or income from a side job. Each of these can be a good opportunity to pay off debts. Pay off the loans that have the highest interest rates first. This means you should focus on the debts that cost you the most money in interest. This way, you can save money and improve your credit score.

By using extra money to pay down your debt, you can reduce what you owe and build a more secure future. Whether it’s a one-time cash influx or regular extra income, having a plan to manage these funds wisely can help you feel financially free and at ease.

To make the best use of this extra cash, think about dividing it into three helpful categories:

- Paying Off Debt: Use a big part of this money to pay down any debts you owe. Pay off the debts that have high interest rates first, which can save you a lot of money in interest over time and help you feel more financially secure.

- Enjoy Yourself: Keep a small amount for fun things to keep you motivated.

- Save for the Future: Save another part for your future needs to make you more secure.

This balanced plan helps you feel good about dealing with debt while also enjoying life and preparing for what’s ahead.

An Awesome Guide To Rebuild Fantastic Financial Life For Beginners

The Emotional Side of Debt Payoff (This Is Where Change Really Happens)

Paying off debt can improve people’s emotional and personal well-being in addition to their financial situation. Many people who strive to pay off their debt claim that doing so improves their happiness in a number of ways. The following are some of the main psychological advantages of debt repayment:

– Less Anxiety: – Having debt frequently results in a great deal of tension and anxiety. Having debt can put a lot of strain on you. On the other hand, people typically experience less stress when they begin to pay off their debt. Every time they make a payment, the financial strain is reduced, which calms them down and elevates their mood.

Improved Sleep: Concerns about money might frequently keep you up at night. The burden of debt makes it hard to relax. As you lower your debt, you might find it easier to sleep well. When you’re less stressed about money, you can rest better, which gives you more energy for the day.

– Increased Confidence: Paying off debt boosts your self-esteem. When you achieve your goal of becoming debt-free, you feel a sense of accomplishment. This success can help you trust your ability to make good choices with money and other areas of your life. This newfound confidence allows you to make better decisions and set new goals.

– Better Problem-Solving Skills: You begin to confront your financial issues rather than ignore them as you work to pay off your debt. This teaches you how to keep an eye on your expenses, build a budget, and make wise decisions. By addressing financial concerns head-on, you may take control of your money and achieve better stability and success.

Hope for the Future: You can feel more optimistic and energised after paying off debt. Every action you take to lower your debt can improve your outlook on life. This optimistic perspective can motivate you to seek out new chances, make educational investments, or establish long-term, fulfilling goals.

In conclusion, paying off debt has many emotional benefits that go beyond just making your finances better. It can lessen tension, enhance sleep, increase self-assurance, boost your confidence, encourage better money management, and make you feel more hopeful about the future—all of which can help you grow as a person.

Ultimately, the process of paying off debt empowers individuals. It helps them transition from simply reacting to financial challenges to actively managing their money in a positive way.

Common Debt Payoff Mistakes to Avoid

- Ignoring minimum payments

- Using credit for emergencies instead of savings

- Trying to be perfect

- Comparing your journey to others

- Giving up after setbacks

Setbacks are part of progress.

A Simple Debt Payoff Plan (Quick Recap)

- Know how much you owe

- Make your money situation stable.

- Decide on a way to pay off debts (snowball or avalanche)

- Pay the minimum amounts and put extra money towards your biggest debt

- Use automatic payments whenever you can

- Keep doing it regularly

- Change your plan if your life changes

- That’s all! It may be simple, but it can still be hard. You can do it!

That’s it.

Simple doesn’t mean easy — but it does mean doable.

Related articles:

How To Stop Living Paycheck To Paycheck

How To Build An Emergency Fund

Conclusion — Debt Freedom Is Built Quietly

Getting out of debt takes time and careful planning; it won’t happen fast.

To pay off debt, you should follow a clear step-by-step plan and make regular payments. With each payment, you get closer to your financial goals.

Every payment helps you:

– Decrease the amount you owe

– Reduce your worries about money each month

– Improve your overall financial health

It’s important not to rush this process. You don’t need to feel stressed or try to be perfect. What is important is to develop a clear plan tailored to your financial situation and to stay committed to it with determination.

Thank you for taking this step toward improving your financial situation. Recognising your effort helps build confidence in your journey to get out of debt.

Leave a Reply